Market Research

The Big Amazon Vendor Study: Industry Insights & Key Statistics (2024)

Want to know everything there is to know about Amazon Vendor in 2024? You've come to the right place.

So I recently joined forces with the fine folks from Stratably to better understand what keeps Amazon suppliers up at night.

We asked about their business model setup. We asked about their biggest challenges. And we asked about their results from recent vendor negotiations.

Now, the results are in.

And today I'm going to share what we found with you.

Summary of key findings

- Nearly half (44%) of surveyed 1P vendors use a hybrid sales model. Either via their own 3P account (25%) or by using resellers (19%).

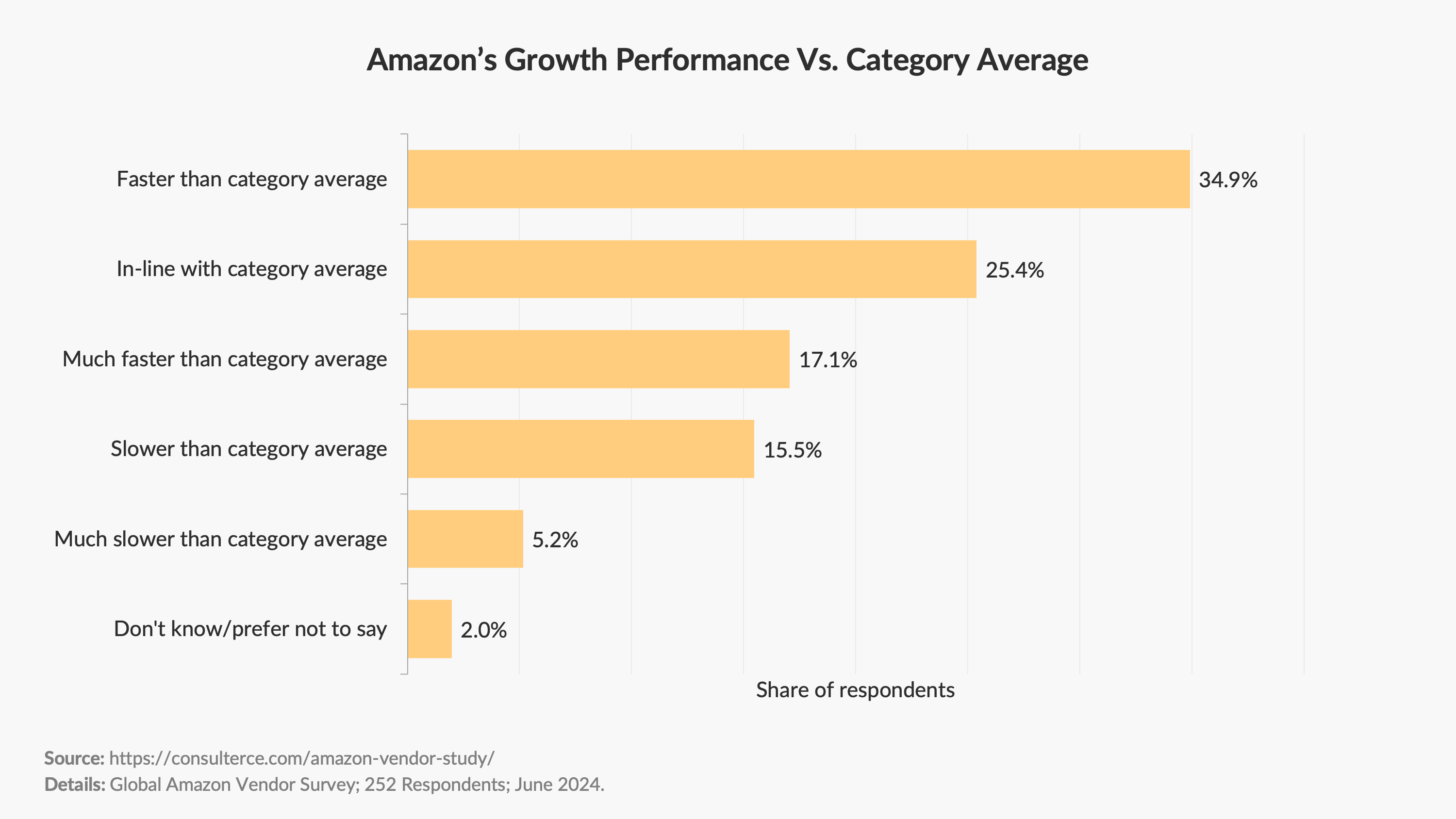

- Amazon remains a growth channel for manufacturer brands, with 77% describing their growth on Amazon as in-line or above the category average.

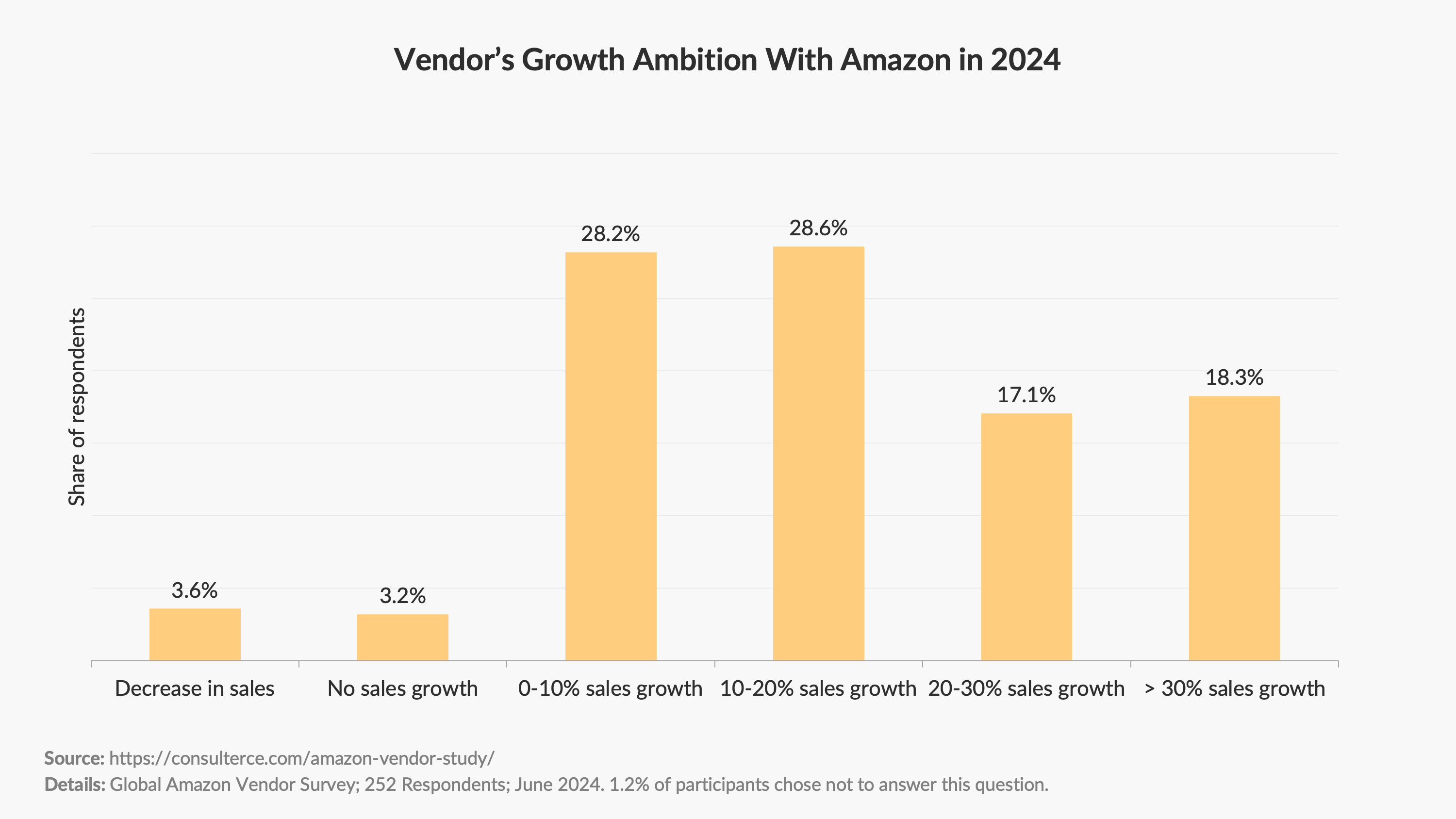

- Vendors expect moderate sales growth with Amazon in 2024, with 28% targeting growth of 0-10% and a further 29% targeting growth of 10-20%.

- Price control and competition are the biggest challenges for 1P brands when selling to Amazon.

- Annual vendor negotiations continue to be time-consuming for brands. 43% of vendors state that negotiation cycles last between 1 and 3 months, while 32% report a negotiation length of 3 to 6 months.

- Joint Business Plans remain transactionally focused. 39% of surveyed vendors stated discussions to be challenging, time-consuming, unsuccessful, or unresolved.

- Annual trade negotiations resulted in lower margins for 35% of vendors, while 40% saw no change in their profitability.

- Most suppliers (56%) yield similar or higher profit margins with Amazon than other retailers.

- Trade terms with Amazon rose by an average of +0.69% YoY in 2024.

- The average Amazon Vendor Service (AVS) programme investment was 2.53% in 2024.

- Financial disputes affect up to 5% of revenue for 87% of surveyed Amazon vendors.

- Current focus areas for Amazon vendors are i) optimizing advertising and promotional strategies (26%), ii) improving forecasting and inventory management (19%), and iii) adapting organisational structures to better serve Amazon (16%).

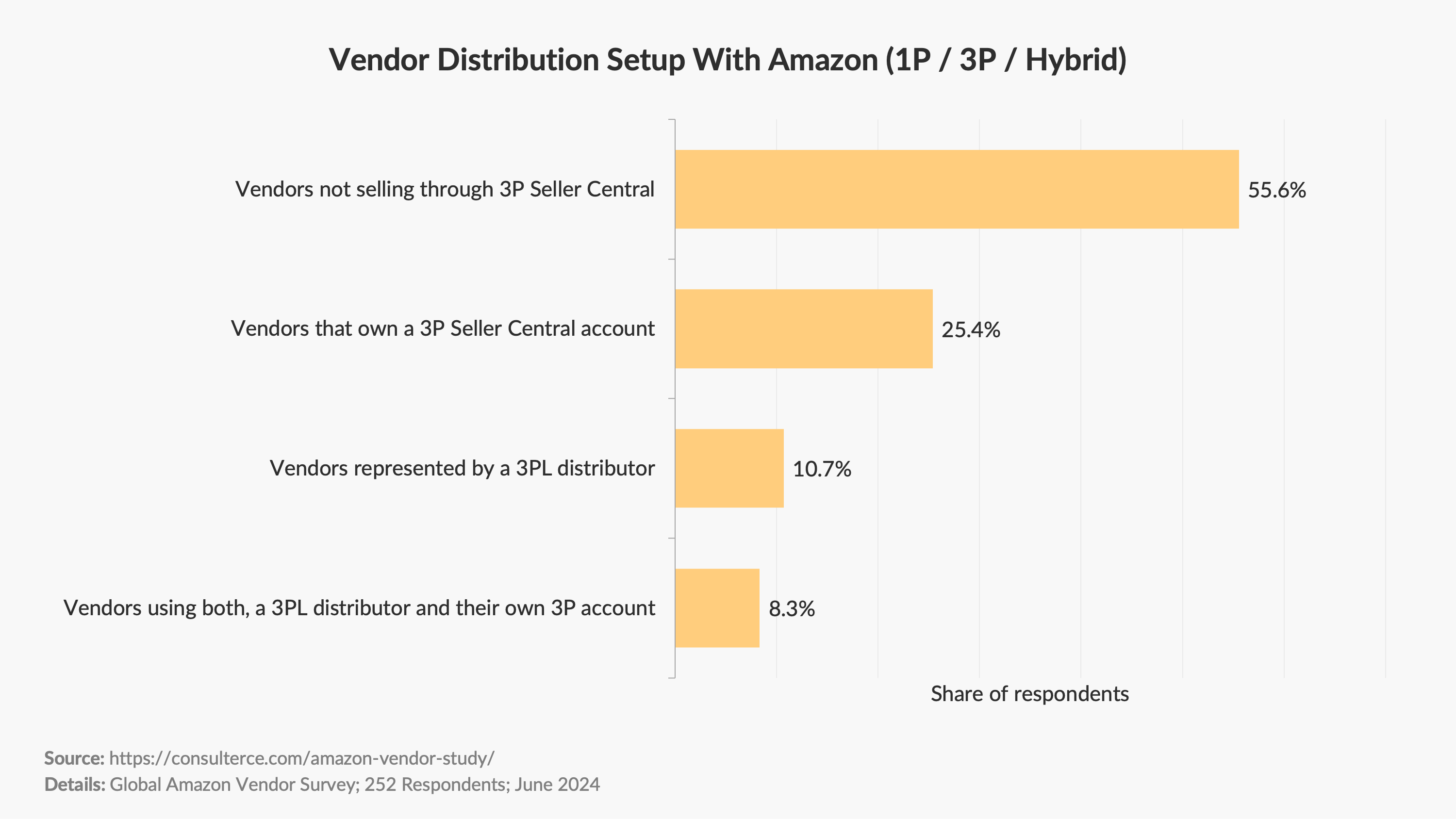

Nearly half of 1P vendors use a hybrid sales model

Whether it's product delistings, Buy Box suppressions, or difficult vendor negotiations. There are plenty of reasons why brands want to diversify their sales by opening a 3P account.

While the majority (56%) of vendors follow an exclusive sales model with Amazon, 25% also state to sell through their own 3P Seller Central account. A further 11% used authorised resellers to distribute items on their behalf, while 8% stated that they sell through both resellers and their own 3P account.

Amazon remains a growth channel for manufacturer brands

Thought Amazon would lose its pandemic-driven sales momentum? You might want to think again. Our survey results show that over 58% of brands think otherwise.

25% of brands stated Amazon grows in line with the category average, 35% stated that Amazon grows faster than the category average, and 17% referred to Amazon's growth as much faster than the category average.

Growth targets have moderated among 1P suppliers

Although there have been signs of Amazon reducing its inventory coverage in recent months, most vendors expect sales to grow with the online retailer in 2024.

28% of vendors stated a 0-10% growth ambition, 29% planned with 10-20% growth, 17% expected sales to grow between 20-30%, and 18% of brands budgeted a growth ambition of >30%.

Only 3.2% of respondents stated no growth plans, while 3.6% expected a negative growth scenario in 2024.

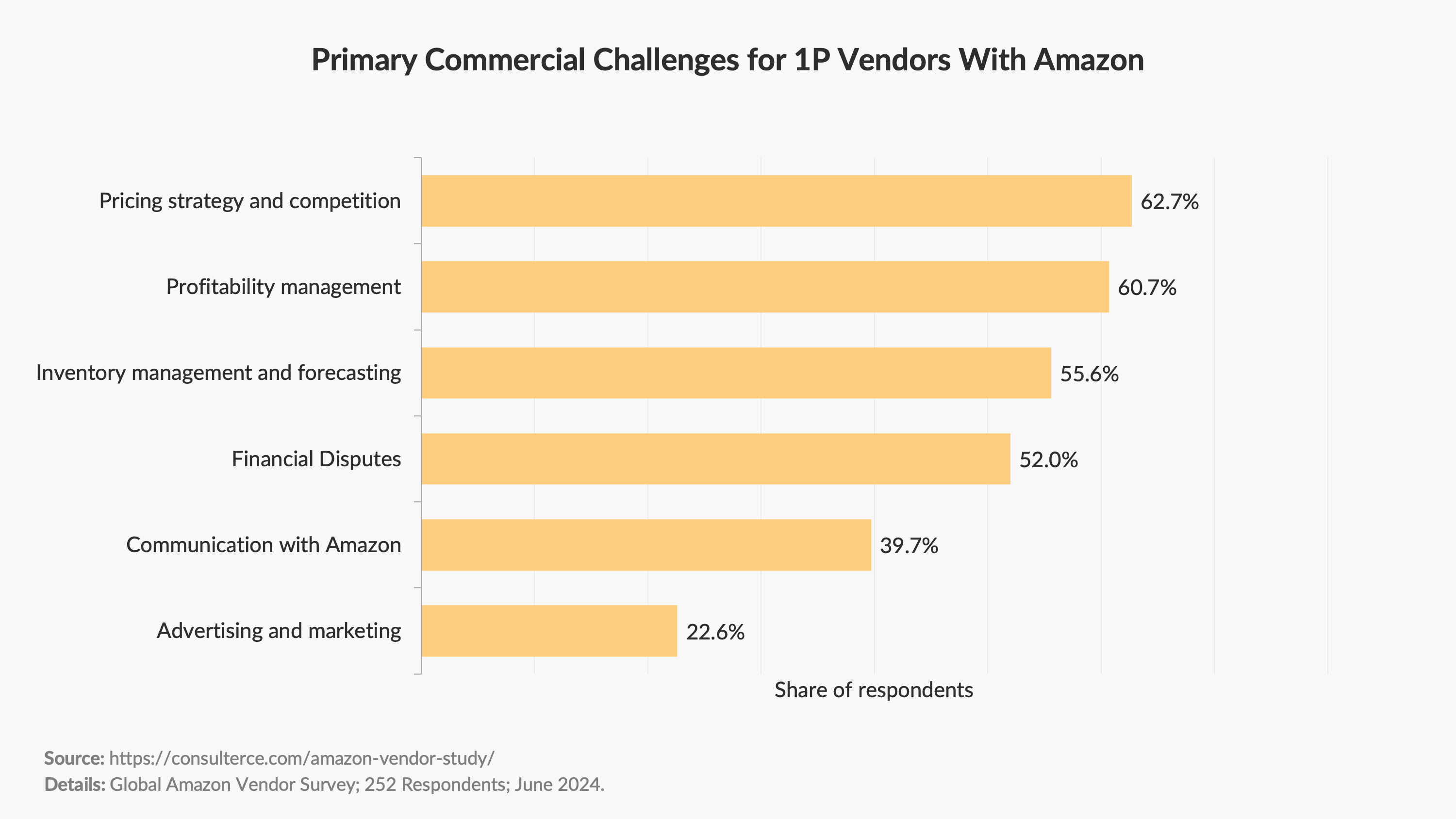

Price control and competition are the top challenges for 1P brands

If you think selling on Amazon has become more difficult over the past year, you're not alone. As the marketplace retailer focuses on reducing its costs to serve customers and making its overall operations more efficient, we're seeing vendors facing more challenges in their day-to-day operations.

Pricing strategy and competition were cited by 63% of brands as a main challenge with Amazon. 61% of survey participants reported difficulties in managing their profitability, while 56% voiced problems in managing their inventory with the online retailer. Communication with Amazon remained a key challenge (40%), despite an overall high Vendor Manager coverage (89% of participating brands had a Vendor Manager assigned to their account).

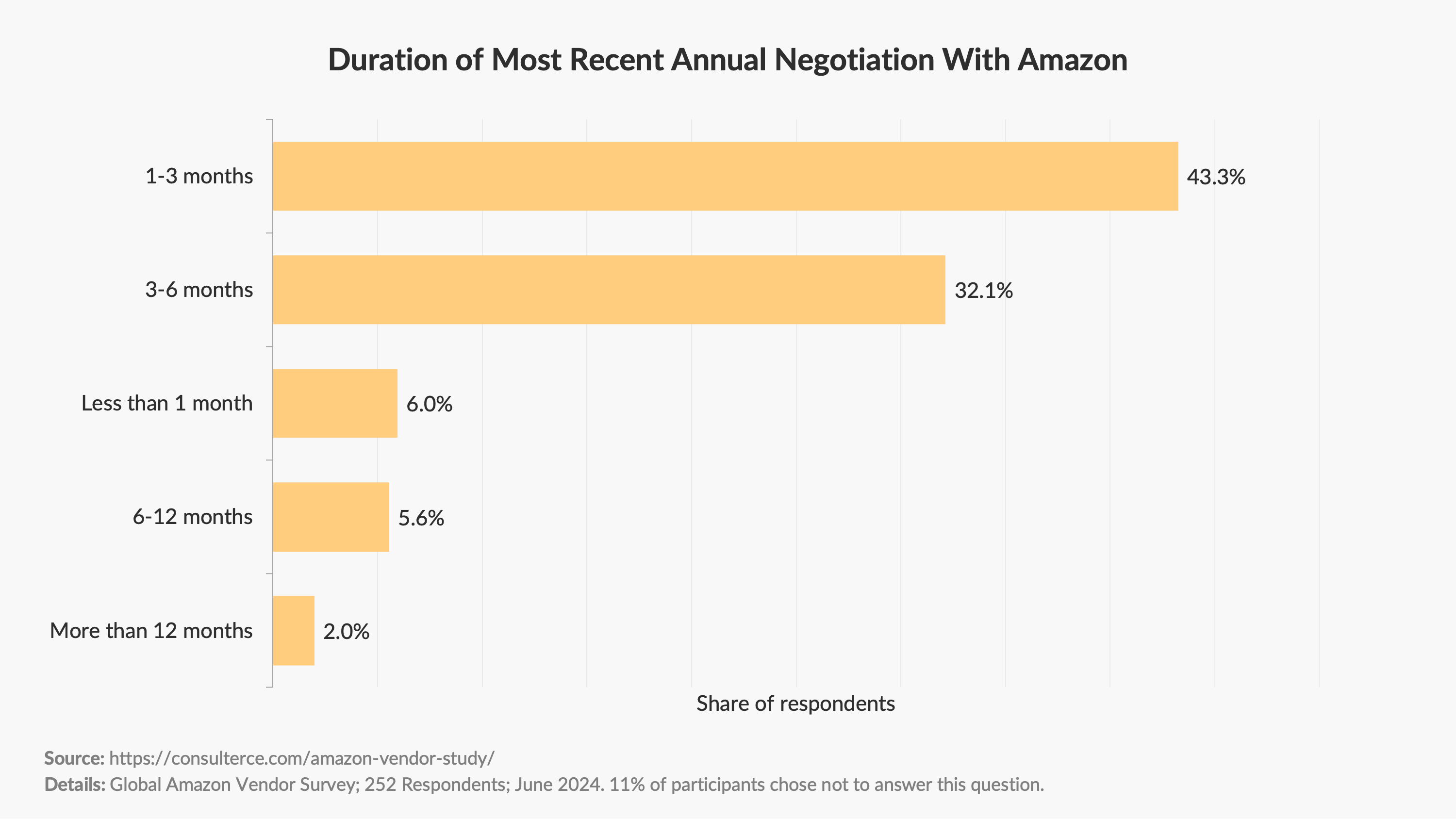

Annual vendor negotiations remain time-consuming

Amazon remained focused on profitability in its negotiations with suppliers in 2024. This was reflected not only in the assertive way in which the Vendor Managers negotiated, but also in the length of annual vendor negotiations.

43% of brands indicated their negotiations took between 1-3 months from start to finish. 32% said their annual trade discussions lasted between 3-6 months. 6% of vendors were in permanent negotiations that lasted between 6-12 months, while only 6% of brands closed negotiations in less than 1 month.

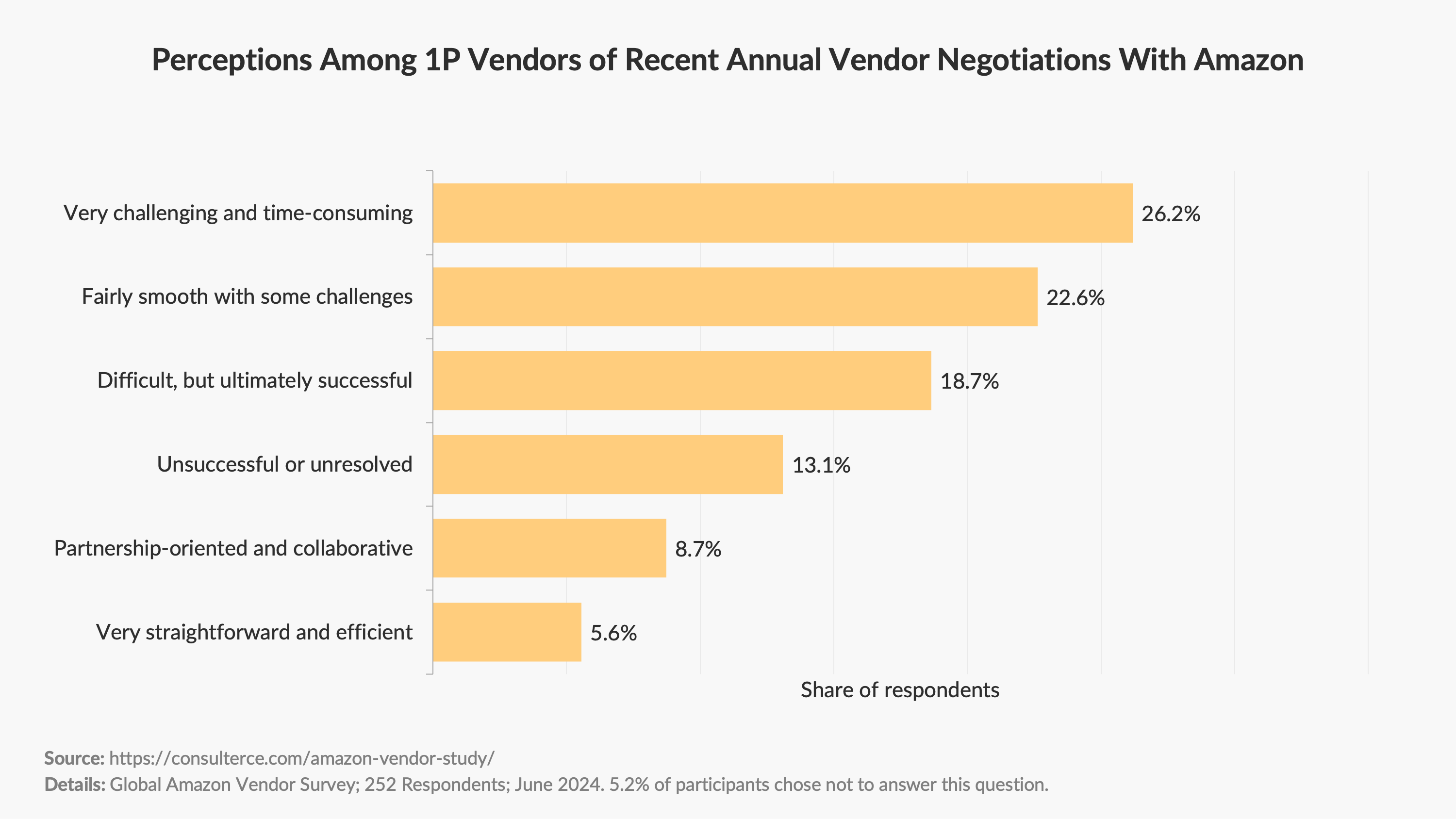

Annual vendor negotiations remain challenging for 1P suppliers

Suppliers negotiating their terms and investments with Amazon continue to view these discussions as a transactional process rather than a true partnership discussion.

39% of surveyed vendors stated annual negotiations were very challenging, time-consuming, unsuccessful, or unresolved. Only 15% of brands stated they found negotiations to be partnership-oriented and collaborative, or very straightforward and efficient.

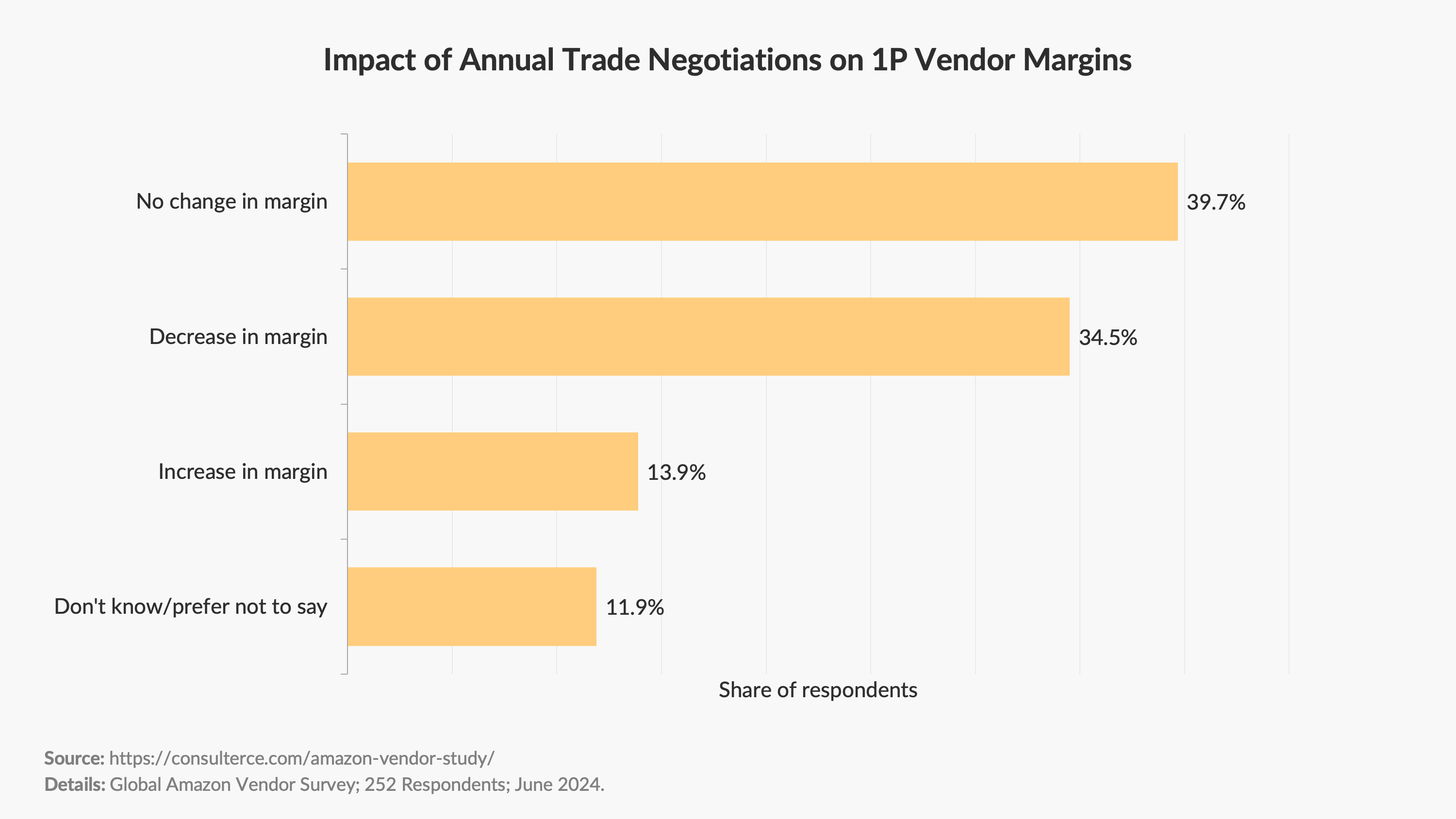

Annual trade negotiations have a direct impact on vendor margins

It's no surprise that there is a clear correlation between annual trade negotiations and the margin of suppliers. After all, these discussions aim to increase the investment of 1P brands.

Yet, the outcome from the most recent annual negotiation cycle varies greatly. 40% of vendors saw no impact on their margins. 35% stated their margins declined following the annual negotiation cycle, while 14% saw an increase in their profitability.

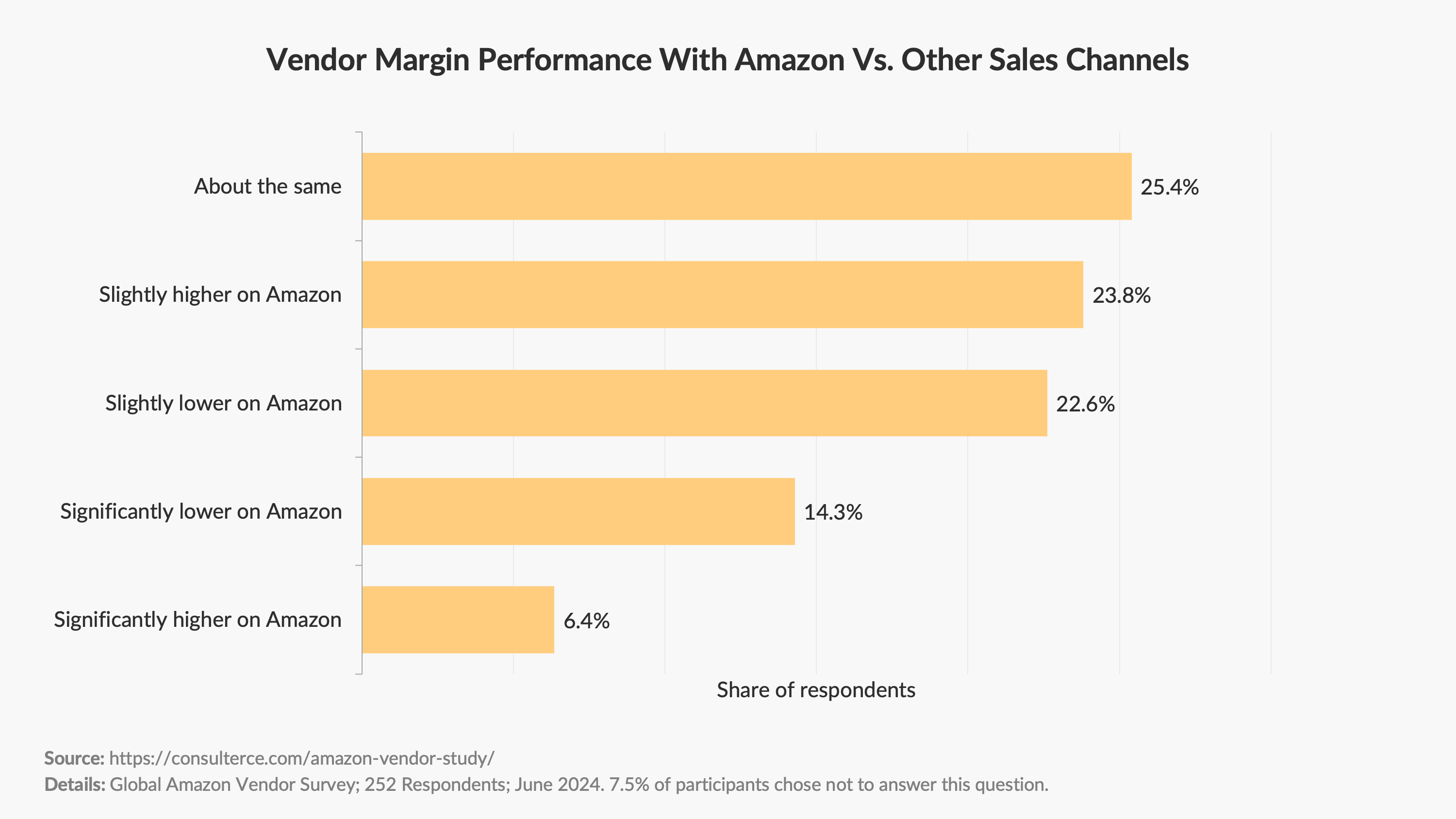

Amazon drives above-average margins for majority of brands

Many agency providers claim that Amazon Vendor Central won't return a profit to brands in 2024. So we put this thesis to the test.

The result rejects this hypothesis clearly. 56% of surveyed vendors stated that their profit margins with Amazon are equal to or above those with other retailers. 23% stated their margins are slightly lower on Amazon, while 14% referred to their profitability as significantly lower.

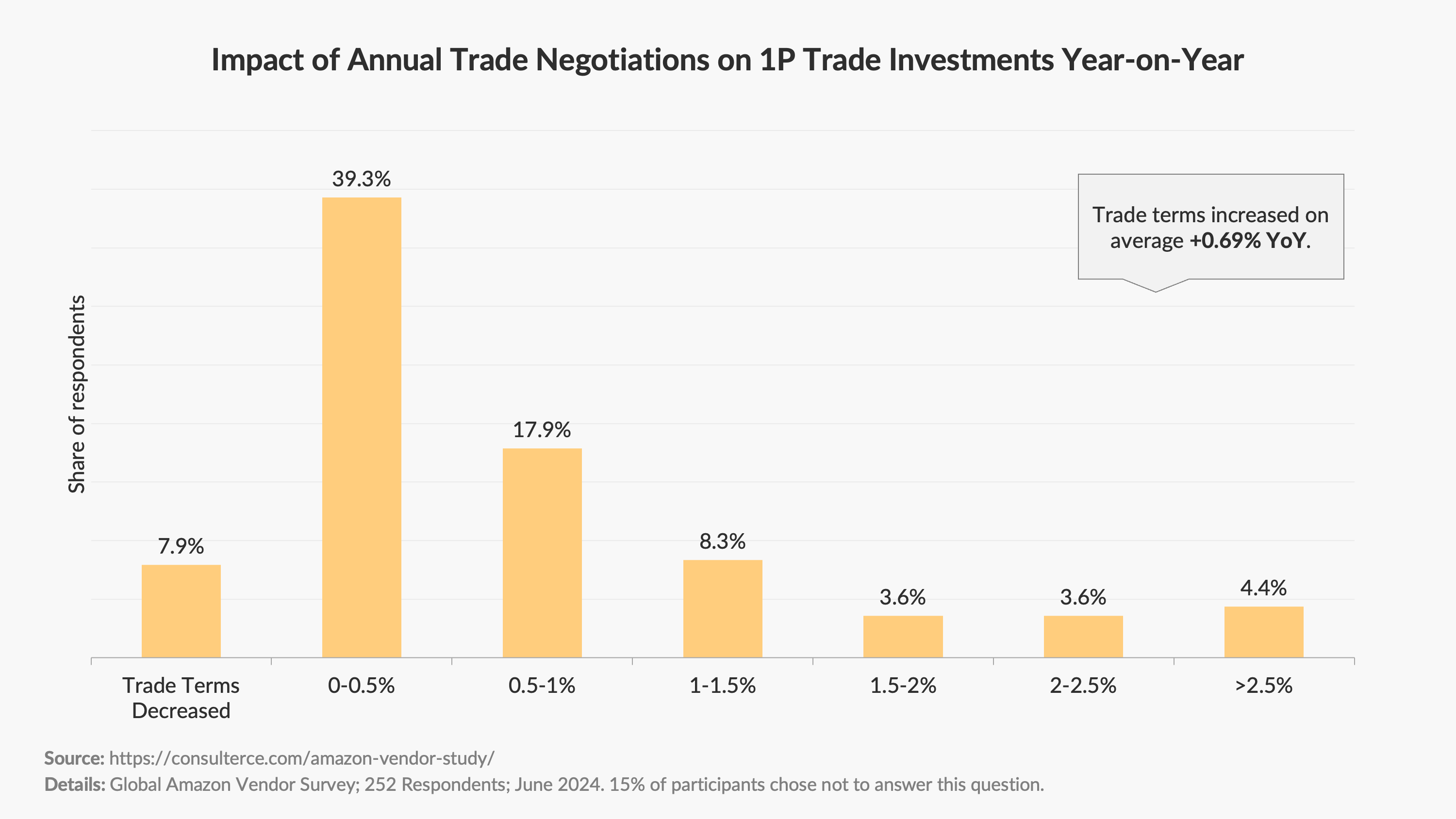

Trade investments into Amazon Retail have increased +0.69% year-on-year

Trade negotiations between Amazon and first-party suppliers once again resulted in a favourable outcome for the online retailer. On average, trade investments rose by +0.69% YoY.

39% of survey respondents reported an increase in trading terms between 0-.5%. 18% of vendors indicated an increase between .5-1%. 8% of brands said their trade terms grew between 1-1.5%. Only 8% of vendors were able to decrease their trade investments YoY.

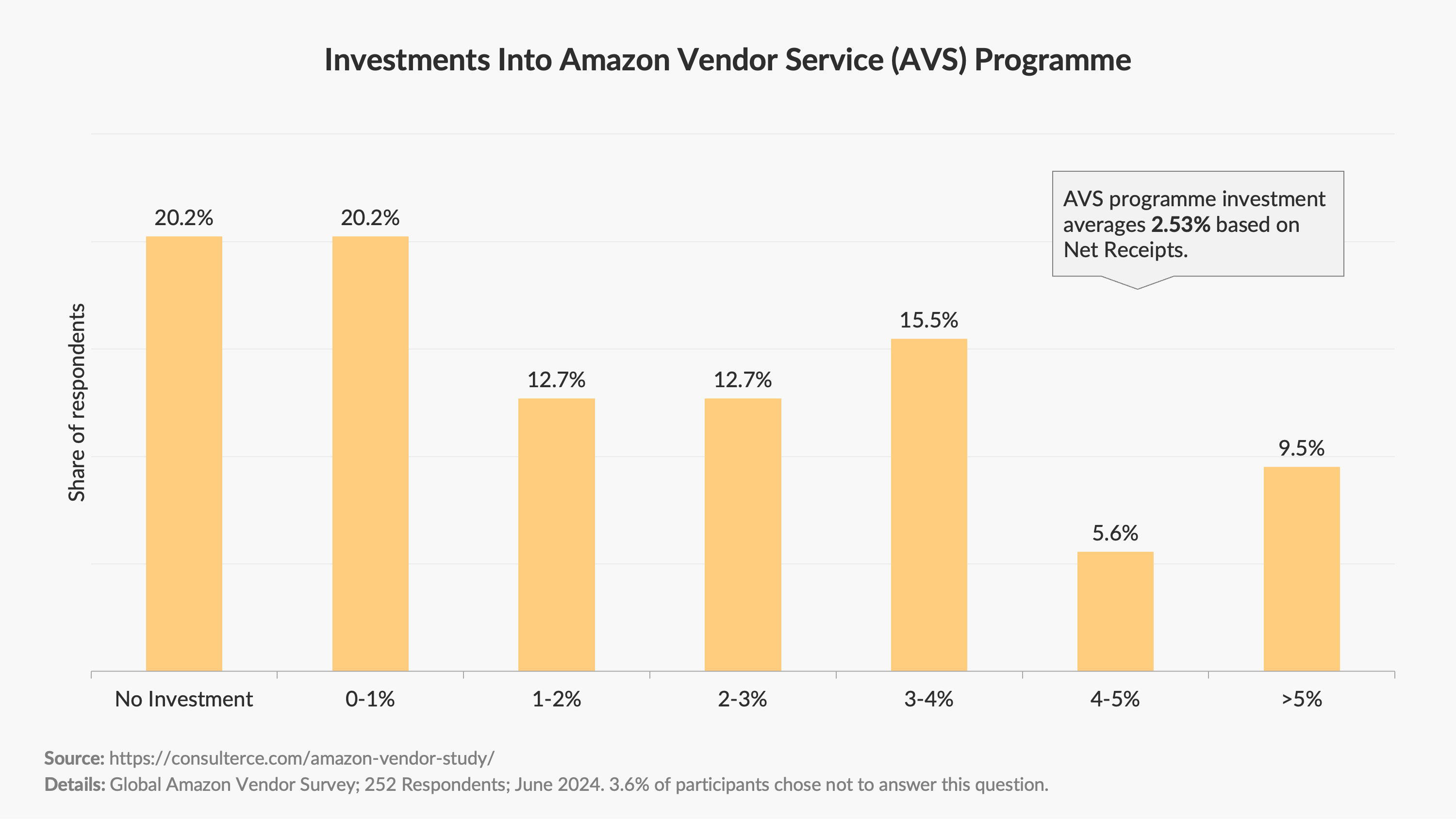

AVS programme investment averages 2.53% in 2024

Although Amazon outsources resources and many brands regularly voice their concerns about the lack of strategic support from brand specialists, the investment into the Amazon Vendor Service (AVS) programme averages 2.53% of net sales across survey participants.

20% of vendors indicated an investment between 0-1% in net sales. 13% of survey respondents indicated an investment between 1-2% and 2-3%, while 15% of brands said they invest between 3-4% into the AVS programme. 20% of brands said they don't invest in AVS.

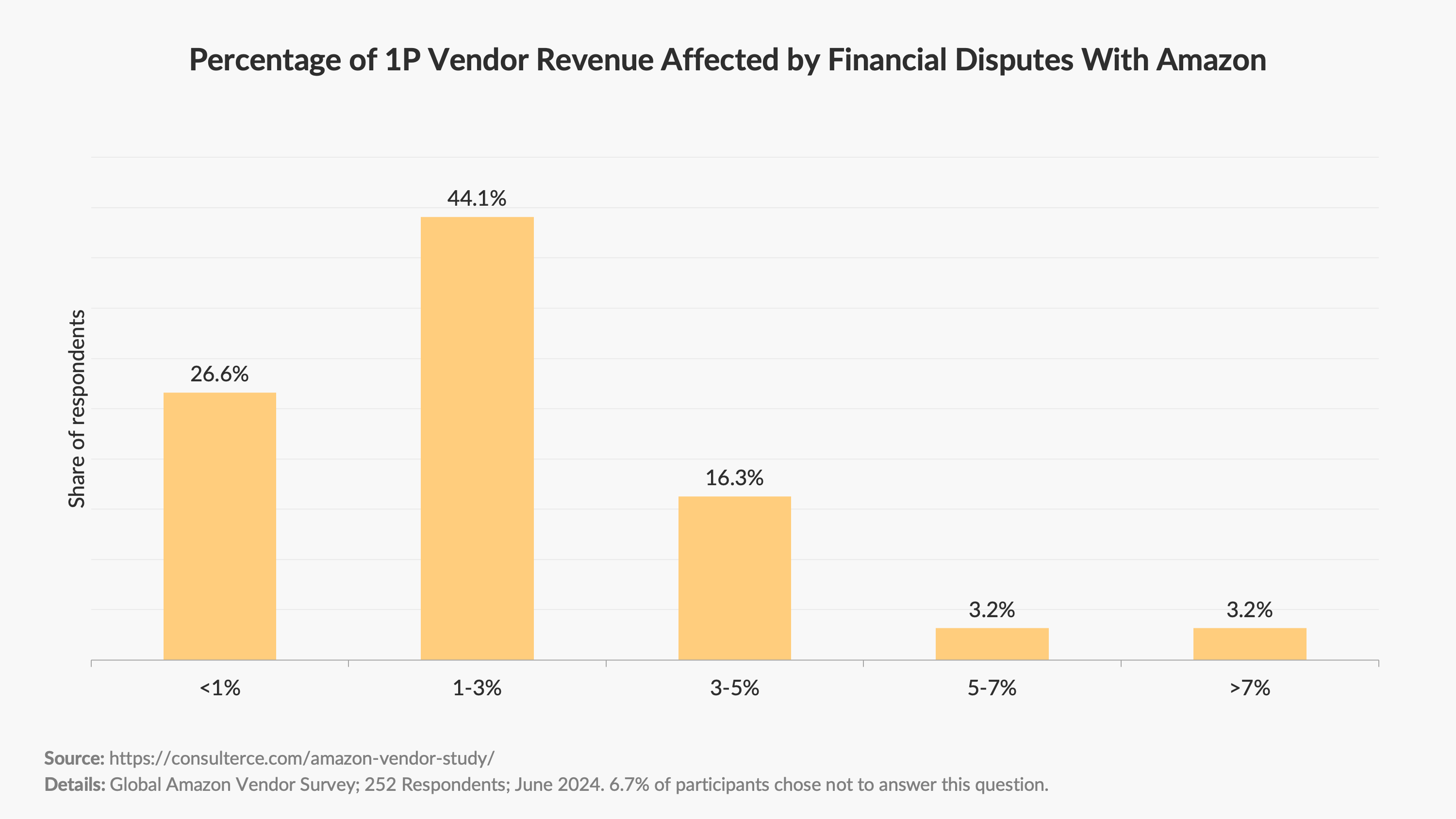

Financial disputes affect up to 5% of revenue for 87% of surveyed Amazon vendors

Catalogue defects plague 1P vendors across product categories. But the magnitude of sales affected by either shortage claims, price discrepancies or other erroneous deductions, where brands have to fight a (lengthy) financial battle with Amazon to get their money back, is significant.

87% of surveyed vendors state that erroneous charges and unpaid invoices affect up to 5% of their Amazon sales. Only 27% of surveyed brands state that financial disputes impact less than 1% of their revenue with Amazon.

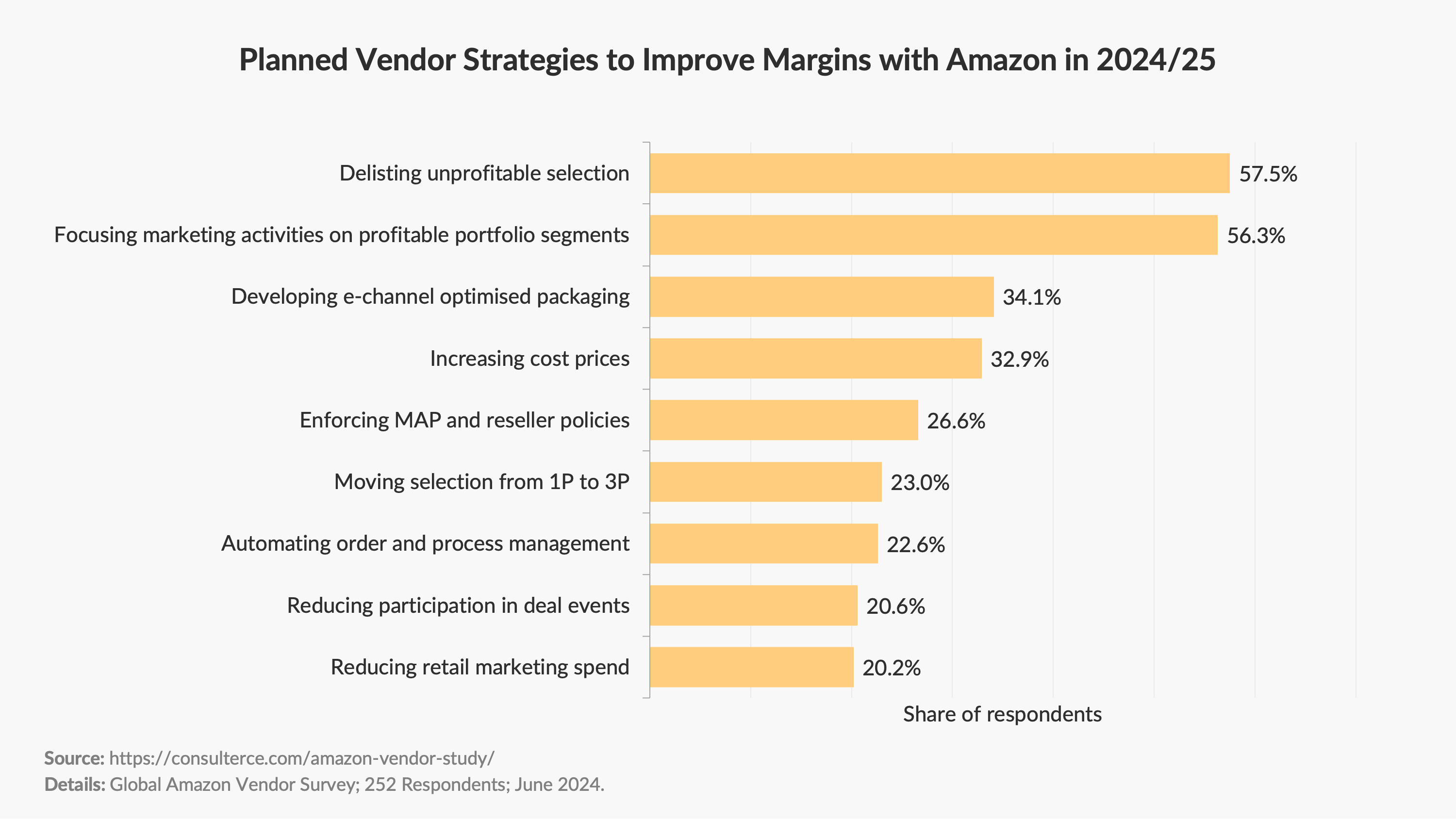

Optimising marketing campaigns, operational processes, and organisational structures are top priorities

Over the last twelve months, Amazon has focused its Retail operation on three areas: Efficiency, profitability, and delivery speed. And it appears that this has clear implications for the priorities of 1P vendors going forward.

58% of survey respondents declared their intentions to delist unprofitable portfolio segments as a key priority to improve their profitability with the online retailer. 56% of brands said focusing their marketing dollars on high-margin items and/or customers will be their focus in 2024.

Developing channel-optimised SIOC/FFP packaging is a focus of 34% of 1P vendors, while 33% intend to raise cost prices with Amazon in the next twelve months.

Conclusion

That wraps up our Amazon Retail study for 2024. I hope you found the data interesting and useful.

If you found value in today's article, please share it on LinkedIn or with your coworkers.

And if you participated in the survey, thank you! Without your contribution, this study would not have been possible.

Background of survey and profile of survey participants

The survey was conducted from April to May 2024 and targeted representatives of first-party Amazon suppliers. A total of 252 survey responses were recorded. The survey was conducted anonymously.

Vendor business size with Amazon

34% of survey respondents reported annual Amazon sales between $0 and $10 million. 38% of survey respondents reported annual Amazon sales between $10 and $50 million. 13% of survey respondents reported annual Amazon sales between $50 and $100 million. Another 13% reported annual Amazon sales of over $100 million.

Vendor categories of survey participants

25% of survey participants sold items in the Health & Beauty category, 20% were active in Home & Kitchen, 13% sold goods in Grocery, and 9% were manufacturers of Consumer Electronics. The remaining 33% of surveyed brands came from Toys & Games (6%), Pet Accessories and Pet Food (5%), Clothing & Apparel (3%), and other categories (19%).

Seniority of survey participants

The seniority of survey participants ranged from mid-level to C-Suite. 23% of participants said they were mid-level managers, 48% were senior managers, 19% were executives, and 10% were part of the C-Suite or owners of the company.

Geographical distribution of survey participants

The survey participants were located in multiple regions. 46% of respondents were located in North America, 51% in Europe, 1.6% in Asia Pacific, 0.4% in Latin America, and 0.8% in the Middle East and Africa.

Disclaimer

The survey is not and was not sponsored by, run, or affiliated in any way with Amazon.com, Inc. or any of its subsidiaries.