Market Research

Amazon Vendor Negotiation Study: Early Insights and Trends of AVNs in 2025

If you're selling to Amazon, you know that the online retailer remains focused on profitable growth in 2025.

Whether it's demands for cost price decreases or higher trade terms. Vendor Managers are sending extensive requests to 1P brands for margin support.

With Amazon being one of the largest customers for most manufacturing brands, this makes Annual Vendor Negotiations (AVNs) difficult to navigate.

And leaves many suppliers wondering how to structure their commercial strategies.

To find answers, I teamed up with Russ Dieringer and Claire McBride from Stratably. We looked at Amazon's growth, its negotiation focus, and how vendors plan to improve their margins in 2025.

And now it's time to share the results.

Summary of Key Findings

- Amazon remains a growth channel for manufacturer brands, with 77% describing growth on Amazon as faster than the category average.

- Net margins remain healthy for 1P brands. 73% of vendors state that net margins with Amazon are meeting or exceeding set targets.

- Annual Vendor Negotiations continue to be time-consuming for brands. 69% of vendors expect 2025 negotiation cycles to last between 1 and 3 months, while 18% expect a negotiation length of 3 to 4 months.

- 37% of vendors refer to their 2025 trade negotiations as more difficult than in 2024. 43% state no change in the complexity of negotiations. Only 20% consider their negotiations to be less difficult.

- Only 10% of vendors expect their trade terms to decrease in 2025. 39% expect flat investments YoY. 51% of vendors plan to increase trade investments.

- The majority of vendors (64%) have received cost price decrease requests from Amazon.

- Amazon has asked vendors to reduce cost prices by an average of -6.25% YoY.

- 40% of 1P vendors have experienced punitive measures by Amazon before or during the 2025 AVN.

- Amazon focuses negotiation asks on: higher base accruals (45%), increased promotional spending (42%), supply chain improvements (41%), Amazon Vendor Service (30%), and Amazon Business (23%).

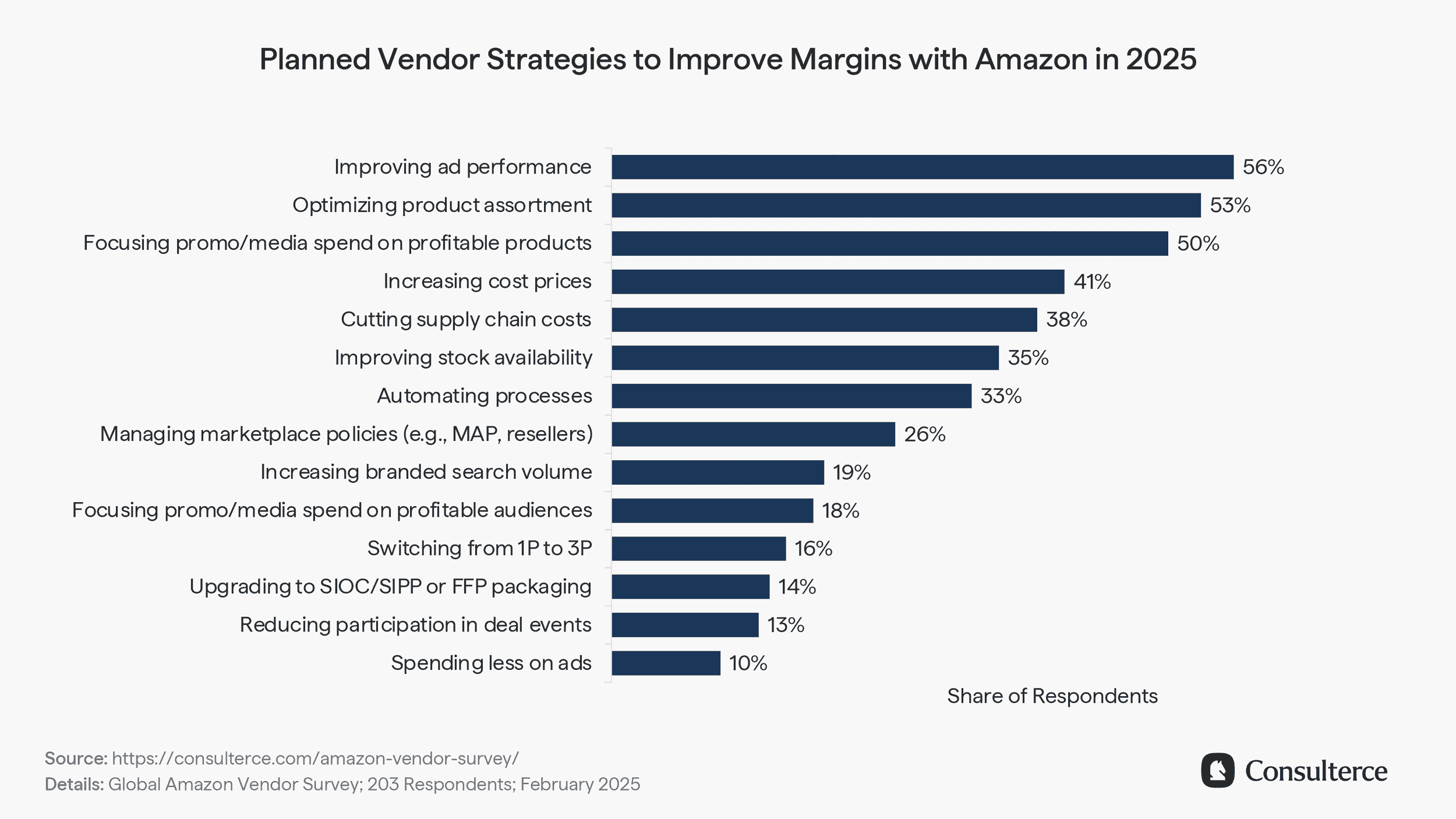

- Key focus areas for vendors are: improving ad performance (56%), optimising portfolio structures (53%), managing profit mix (50%), increasing cost prices (41%), and cutting supply chain costs (38%).

Amazon remains a growth channel for manufacturing brands

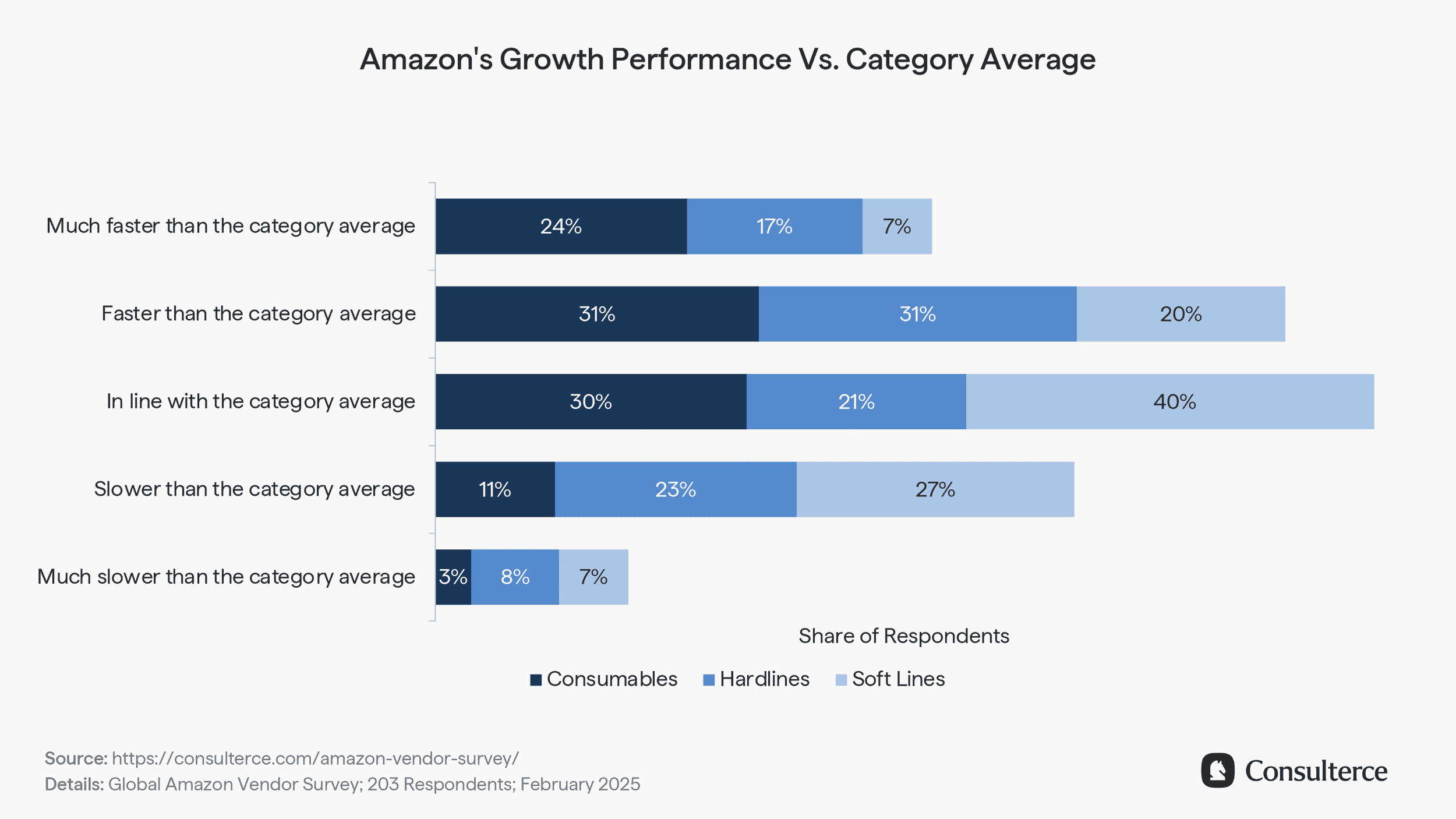

With media headlines focusing on Asian competitors Temu, Shein & Co, it may seem that Amazon is losing its sales momentum. However, a look at our survey results shows that Amazon remains a major growth engine for 1P suppliers.

49% of survey respondents describe their growth with Amazon as above or significantly above the category average. 26% see growth in line with the category average. Only 24% see their Amazon growth performance falling behind their category.

A closer look at the breakdown of these survey results reveals that the dynamics between product categories are very different.

Consumables categories such as Grocery, Beauty, Health and Personal Care, Pets, and Beer, Wines & Spirits continue to be the fastest growing product family on Amazon. 55% of CPG brands see above-average growth with the online retailer, while 30% consider their growth to be in line with category averages.

This is followed by Hardlines categories such as Home, Kitchen, Furniture, Consumer Electronics, Toys and Home Improvement. 48% of Hardlines vendors indicate an above-average sales performance, while 21% see growth in line with category averages.

However, vendors in Softline categories report the biggest loss in sales momentum. Only 27% of suppliers in Luxury, Fashion, and Apparel categories see Amazon growing above category averages.

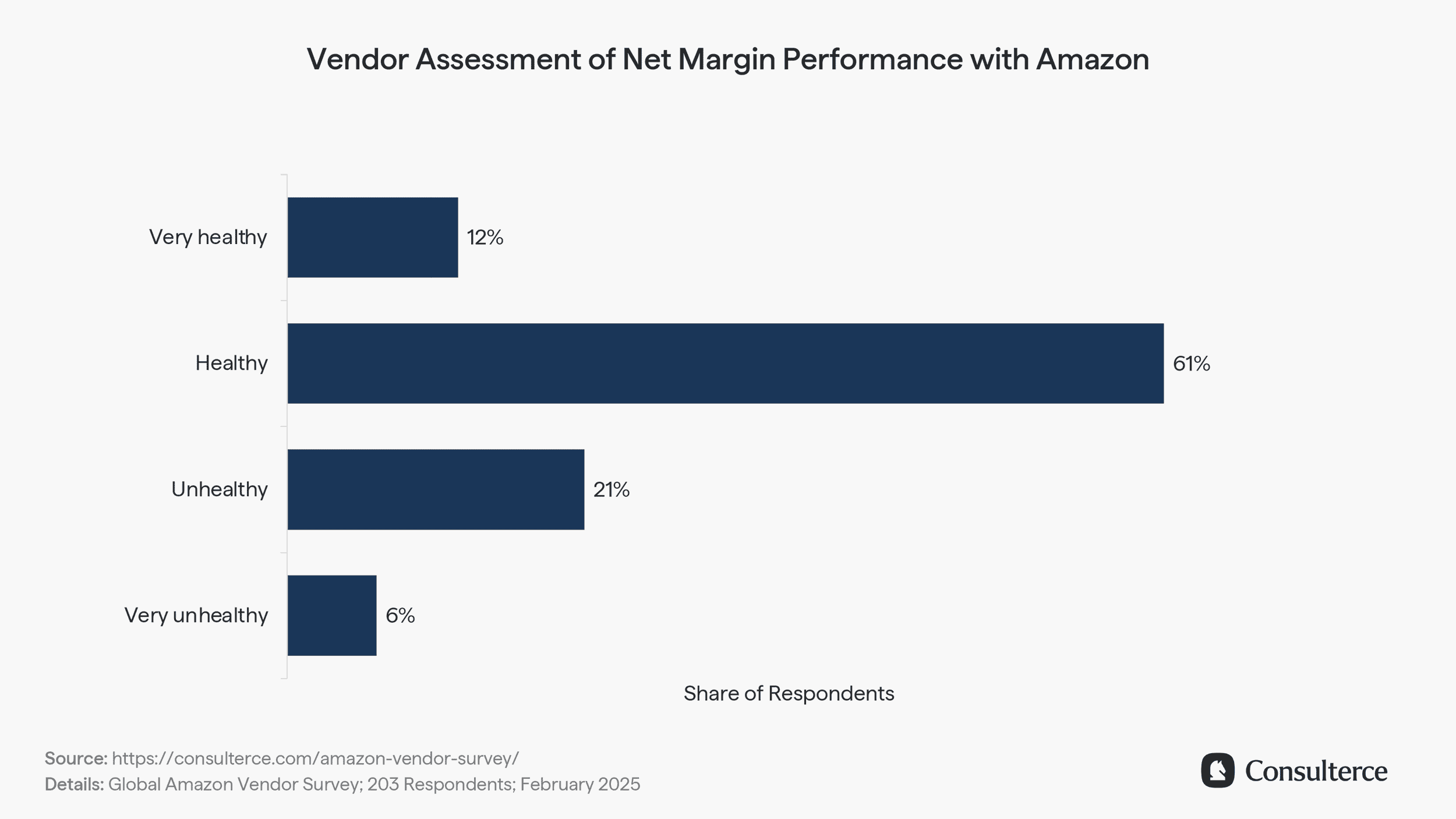

Amazon remains a profitable sales channel for 1P suppliers in 2025

Contrary to popular belief, our research shows that Amazon remains a profitable and accretive sales channel for most 1P vendors.

12% of survey participants stated that net margins are very healthy with Amazon, exceeding internal profit targets.

Another 61% of vendors indicated healthy net margins, stating that profitability meet internal thresholds and set objectives.

21% of suppliers described their net margins as unhealthy, while 6% described them as very unhealthy, thereby missing internally set thresholds and risking the continuation of the trade relationship.

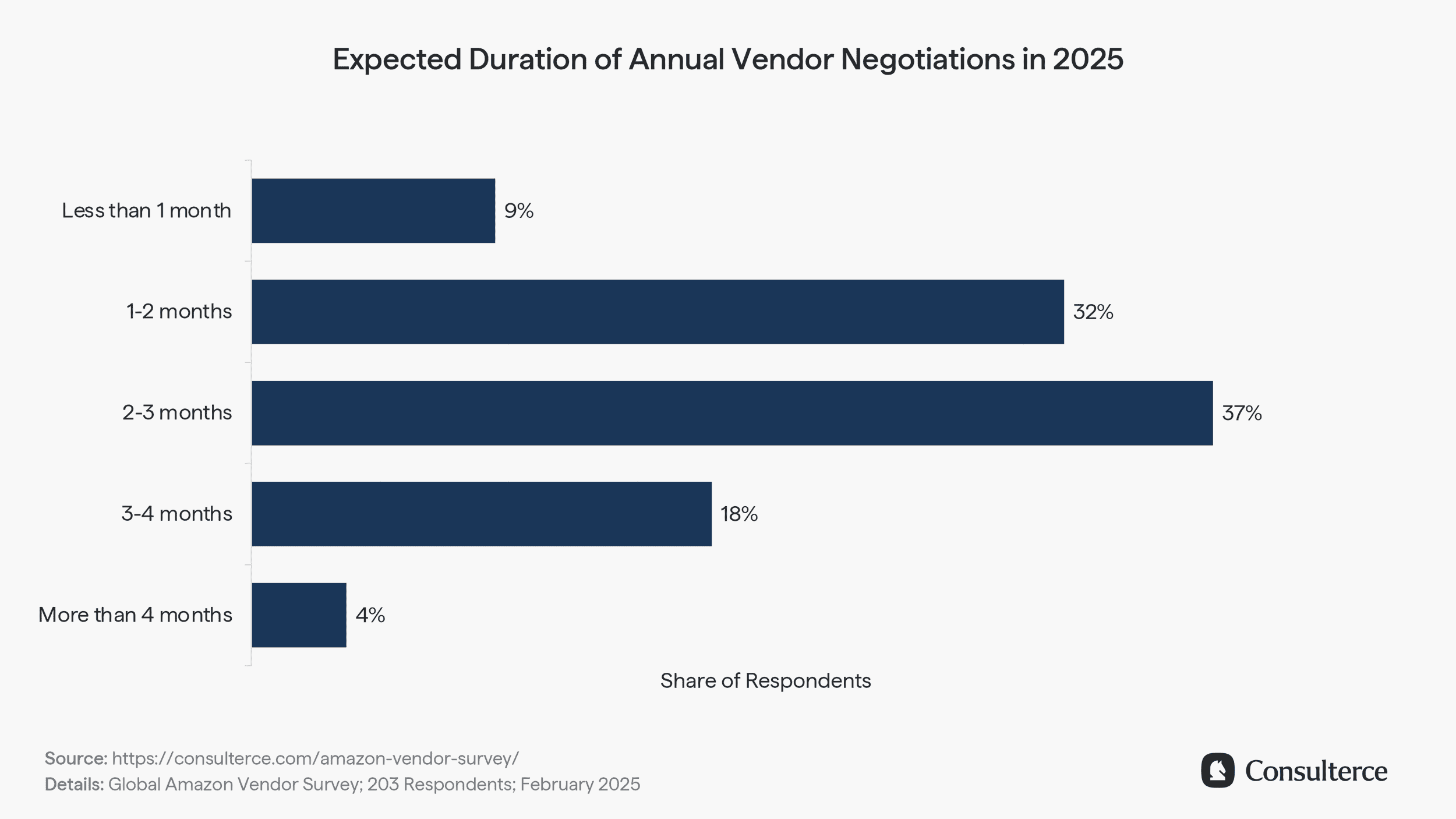

Annual Vendor Negotiations remain time-consuming

Seasoned Amazon negotiators know that it can take several meetings, proposals, and top-to-top escalations to finalise trade negotiations.

Despite Vendor Managers saying they want to speed up the negotiation process, most AVNs are usually not finalised before the end of February.

When asked about the expected duration of their Annual Vendor Negotiation in 2025, vendors stated they they would take an average of 2.6 months. This is optimistic, as our survey results for 2024 showed an actual average duration of 3.5 months.

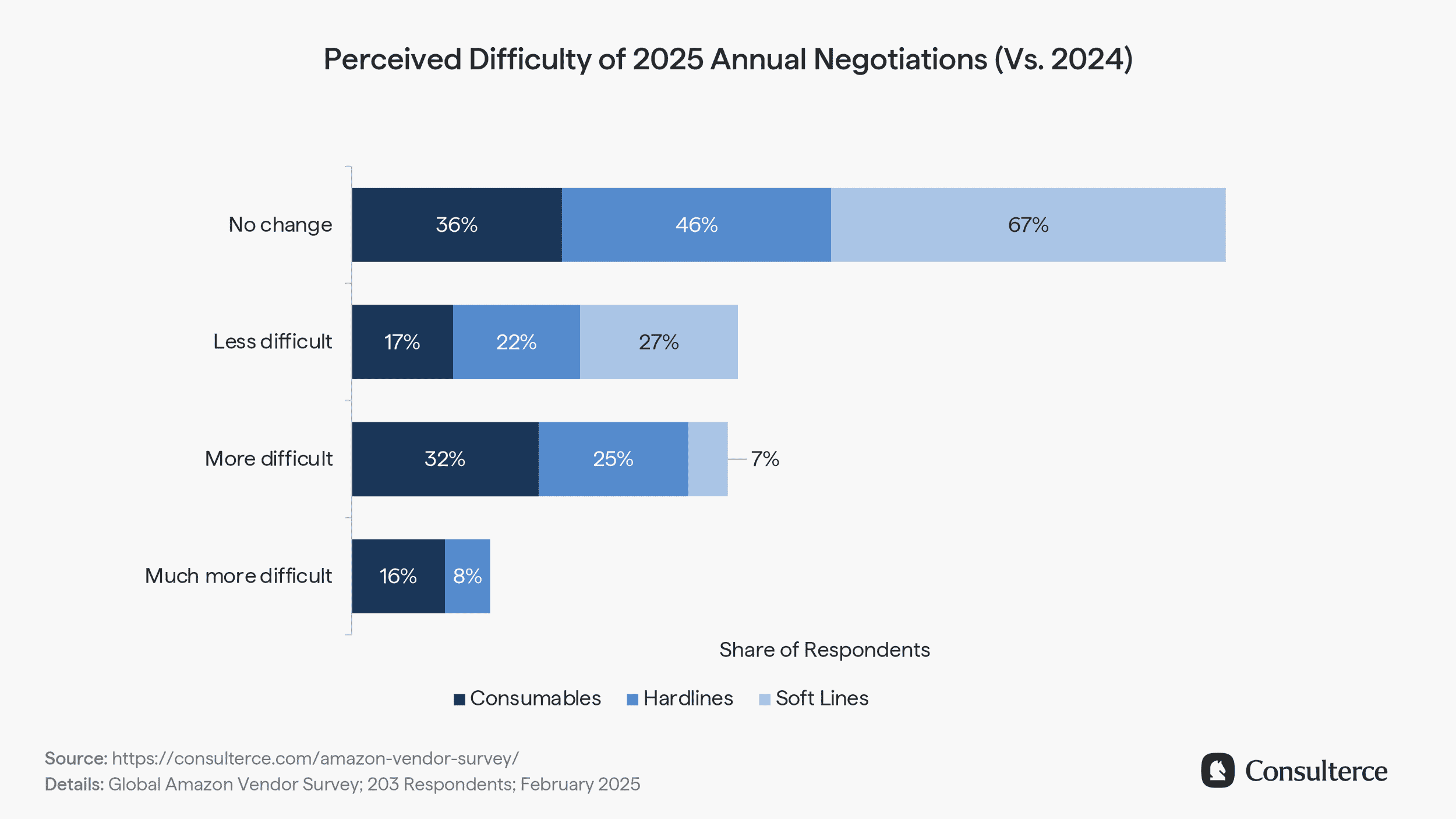

Annual Vendor Negotiations remain challenging for 1P suppliers

Despite the lengthy negotiation process, vendors were generally optimistic about the level of complexity of trade negotiations in 2025. 43% of vendors said the difficulties have not changed, 20% said negotiations are less difficult, while 33% of vendors said they are more difficult than in previous years.

Concern appears to be greater among CPG brands, with 48% stating that negotiations are becoming more difficult, compared to only 33% of Hardlines and 7% of Softline vendors.

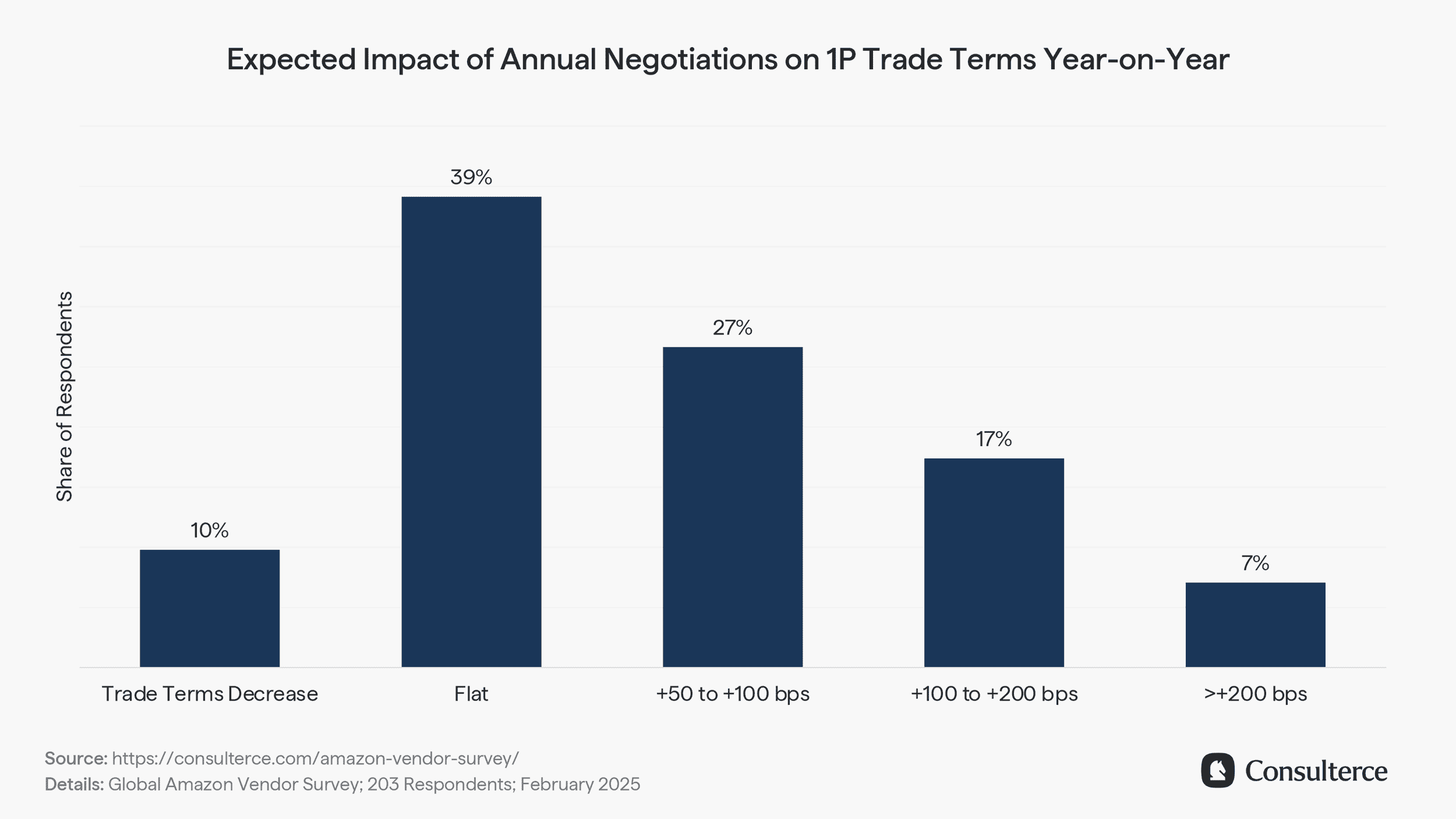

Annual Vendor Negotiations have a direct impact on vendor margins

With Amazon delivering continued growth to 1P vendors, many have prepared their leadership teams to make further concessions on trade investments. Nearly 1 in 2 vendors plan to increase trade terms with Amazon in 2025.

39% of manufacturing brands plan with flat trade terms, while 10% have set a clear target to reduce their exposure into structural trade terms.

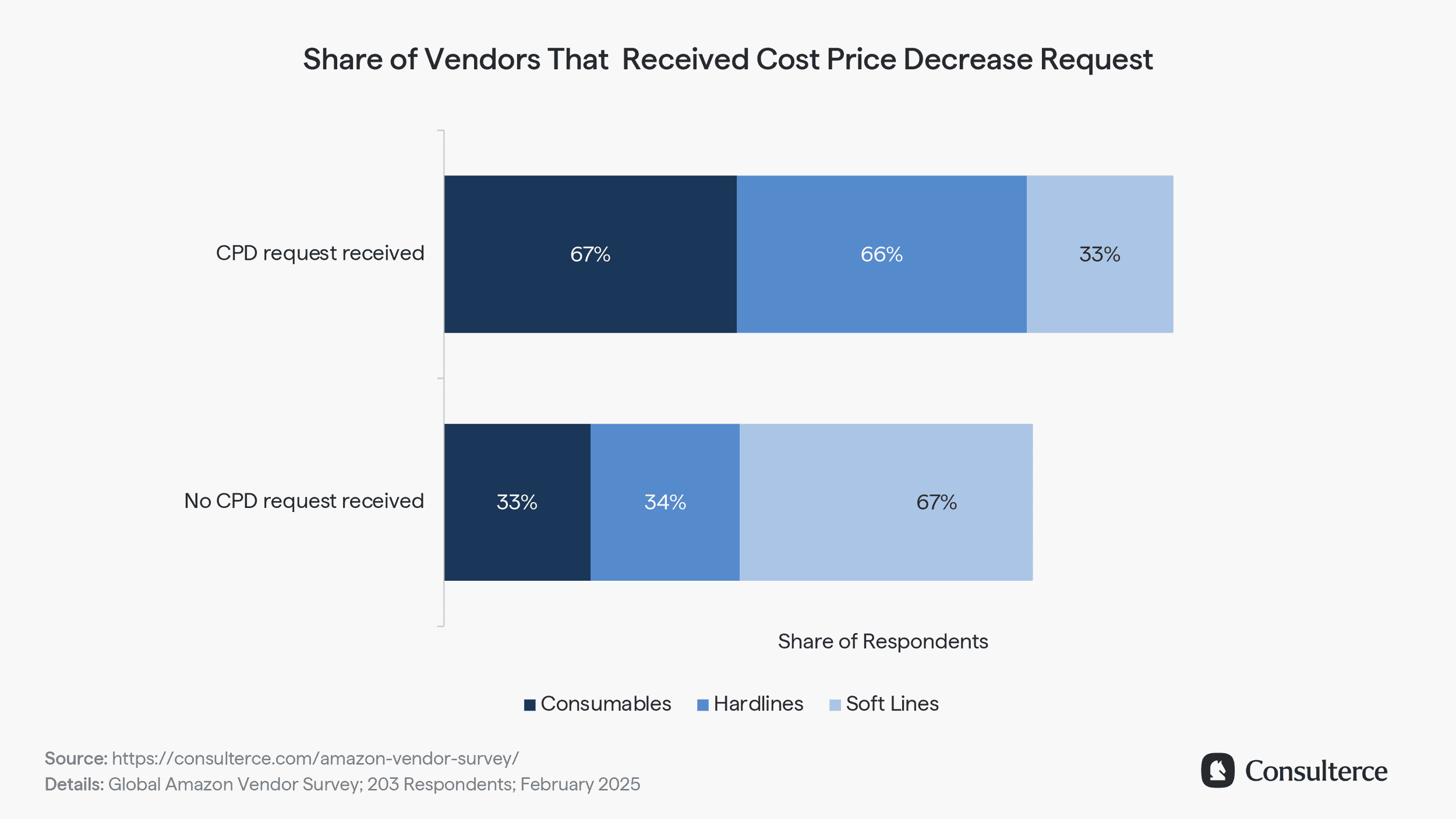

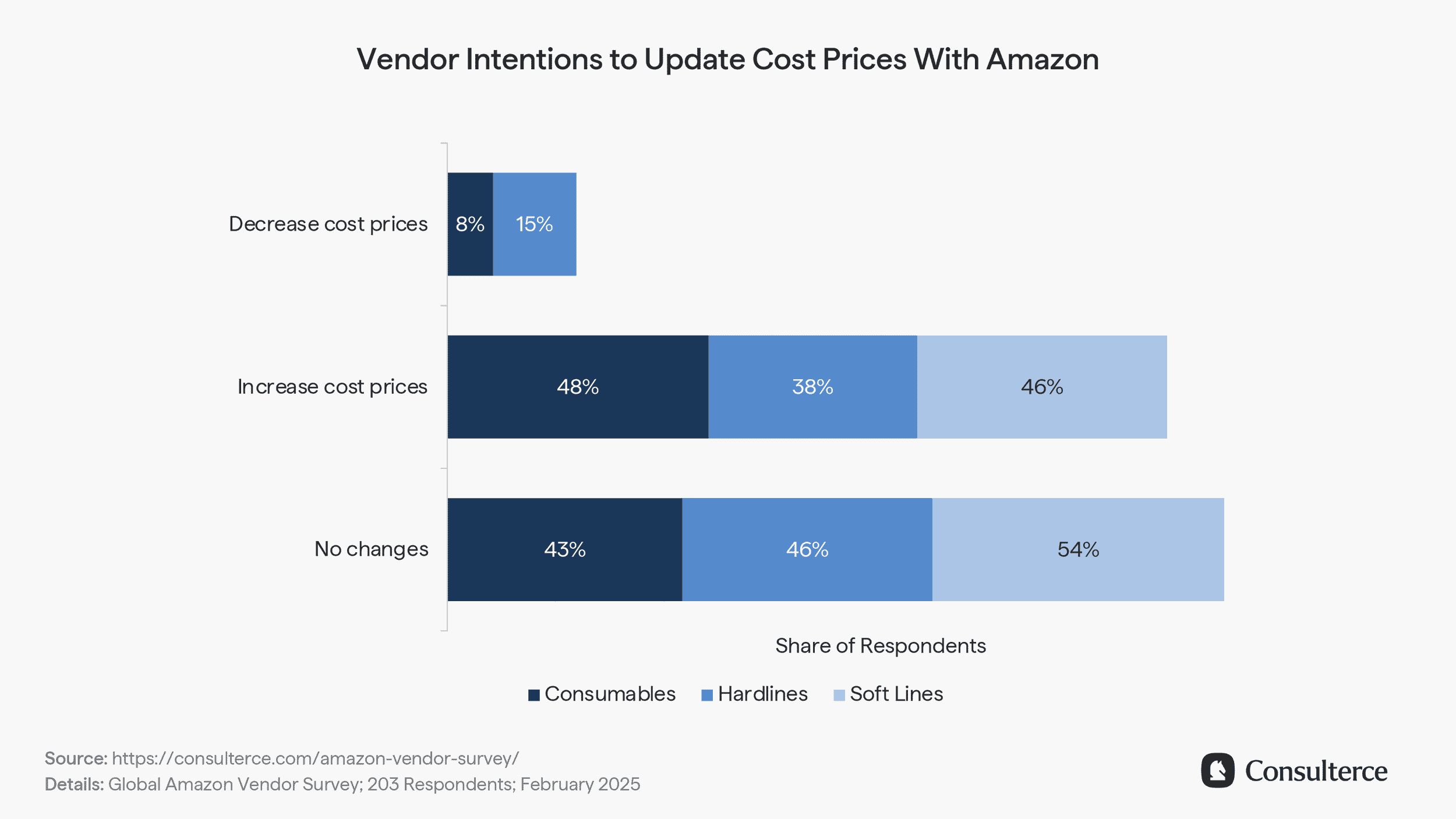

Cost price reduction requests dictate vendor negotiations in 2025

After the pandemic has led manufacturing brands to repeatedly raise cost prices with retailers, Amazon is actively pursuing cost price reductions with 1P vendors in 2025.

67% of surveyed CPG manufacturers stated that they had received requests from Amazon to reduce cost prices. 66% of Hardlines vendors reported the same actions from their Vendor Managers.

Only 33% of Softlines suppliers faced pressure to cut cost prices. This is likely due to the highly seasonal and rotating nature of business in fashion and apparel categories.

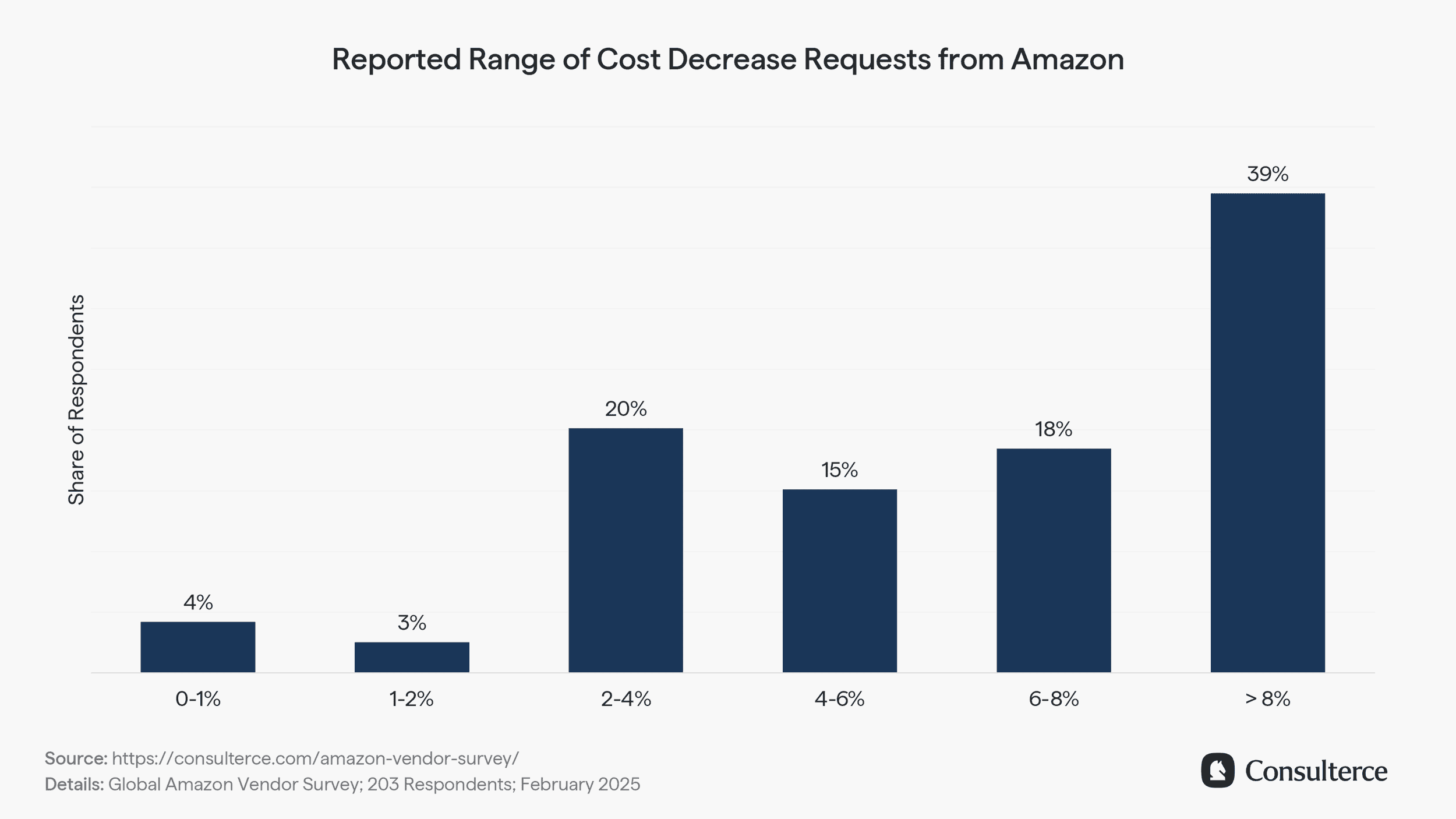

When looking at the reported range of cost decrease requests from Amazon, 53% of surveyed suppliers reported demands for price reductions between 2-8%. 39% of manufacturers reported requests for cost price reductions of 8% or more.

On average, Amazon has asked vendors to reduce cost prices by -6.25% YoY.

But while Amazon is looking to lower its cost prices with 1P vendors, manufacturing brands face the threat of a looming tariff war and an overall volatile trading environment.

Unsurprisingly, 43% of brands surveyed planned to increase cost prices with Amazon, while 45% did not intend to change their cost price base. Only 11% stated that they would consider lowering cost prices in 2025.

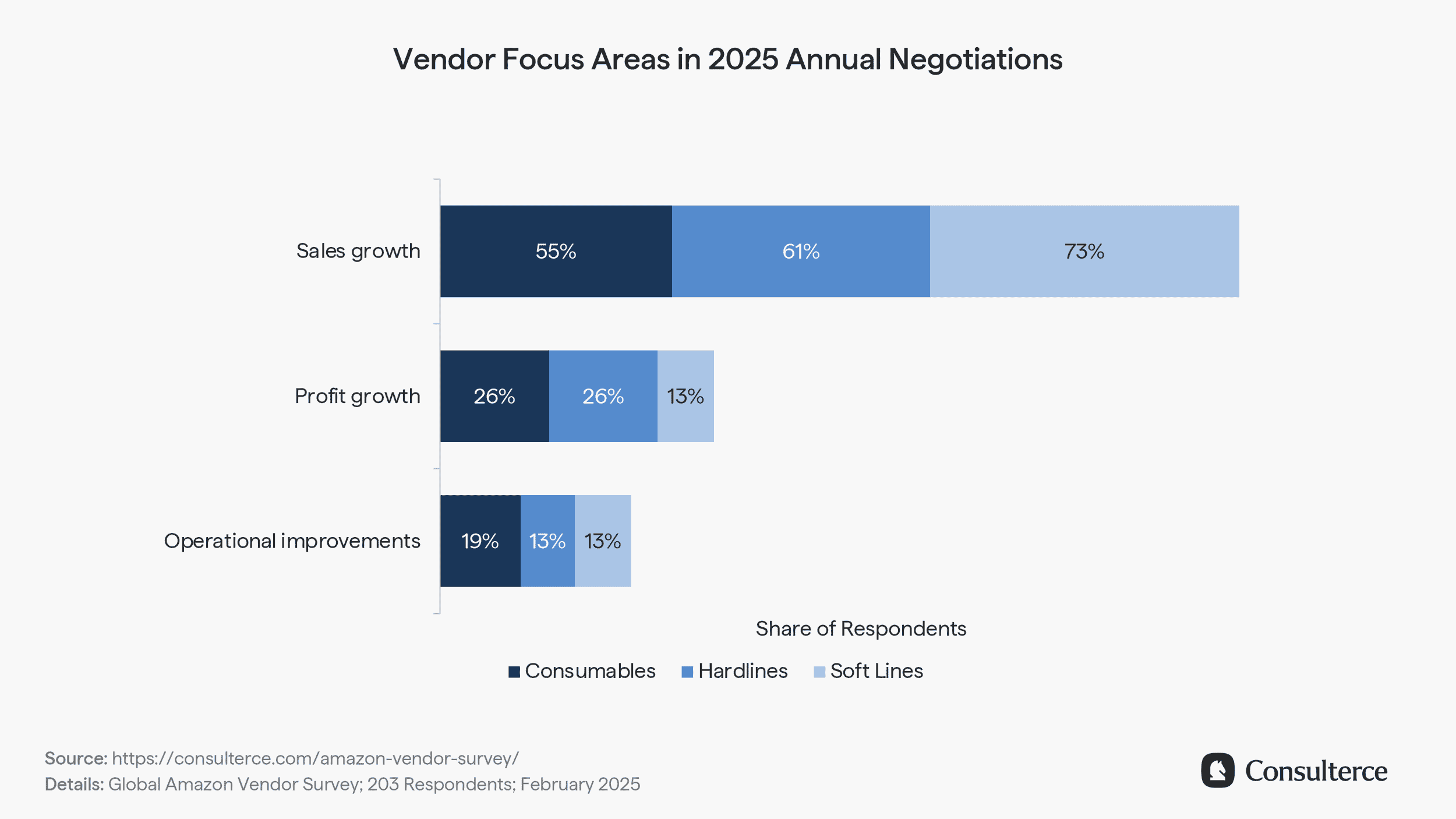

Sales growth returns as the top priority for 1P vendors

Top-line performance has officially reclaimed the crown as the top priority among 1P vendors in 2025. 59% of vendors said that revenue growth is their key focus with Amazon, followed by 25% who want to improve their profit margins. Only 16% of vendor representatives surveyed saw operational improvements as a priority for 2025.

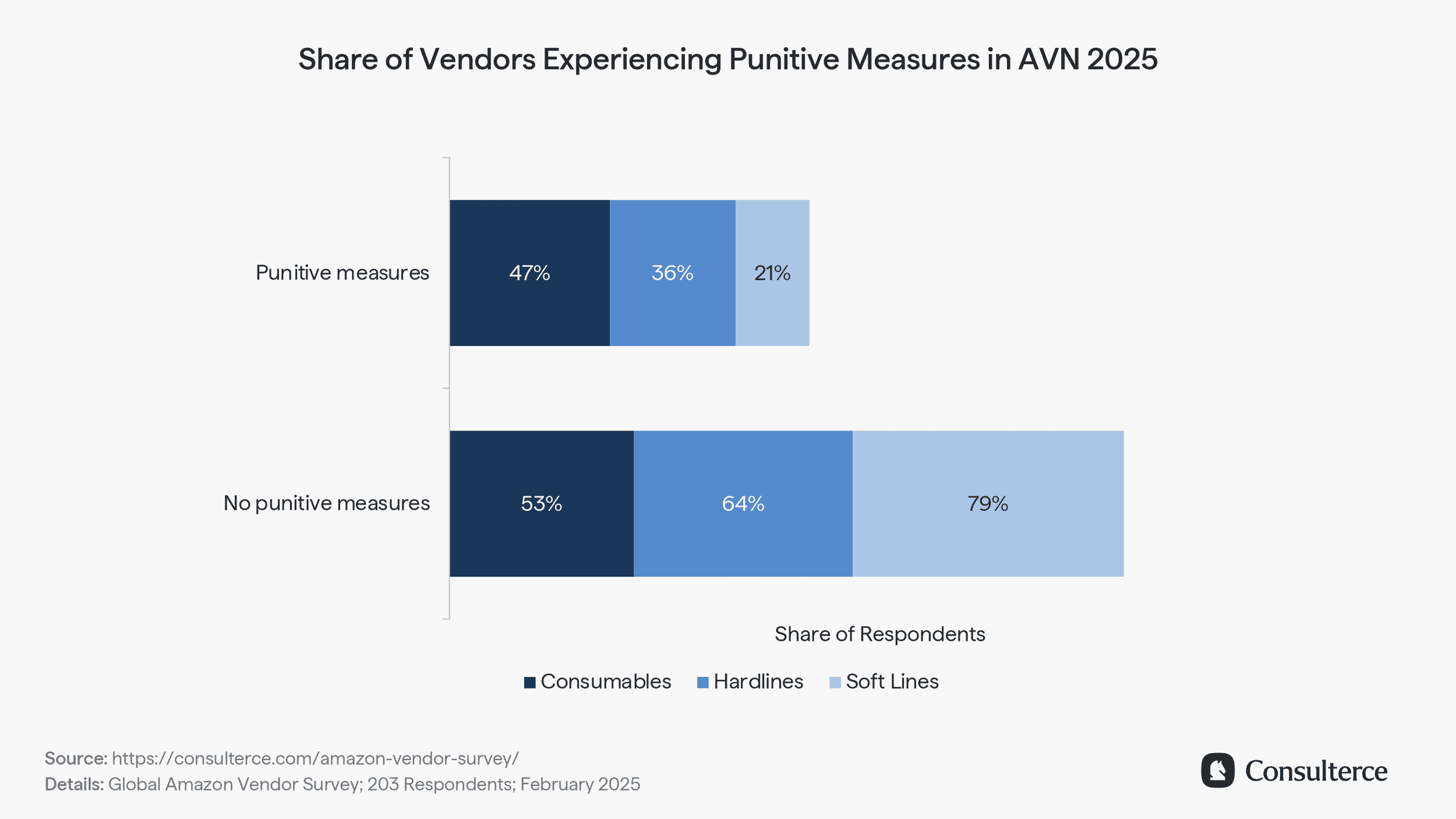

Amazon continues to apply disincentives with 1P vendors to speed up negotiations

Despite efforts to avoid sales disruption, Amazon is known to use complex incentives (also known as punitive measures or disincentives) as part of the AVN process. These include a wide range of actions, ranging from the suppression of the Buy Box to trading stops and the exclusion from deal events.

In the early stages of negotiations, CPG vendors appear to have faced more headwinds from Amazon than brands in any other product family. 47% of Consumables vendors indicated that punitive measures were applied to their account, while only 36% of Hardlines brands and 21% of Softlines vendors reported the same.

Given the end of February deadline for negotiations with French retailers, this percentage is expected to increase in the coming weeks.

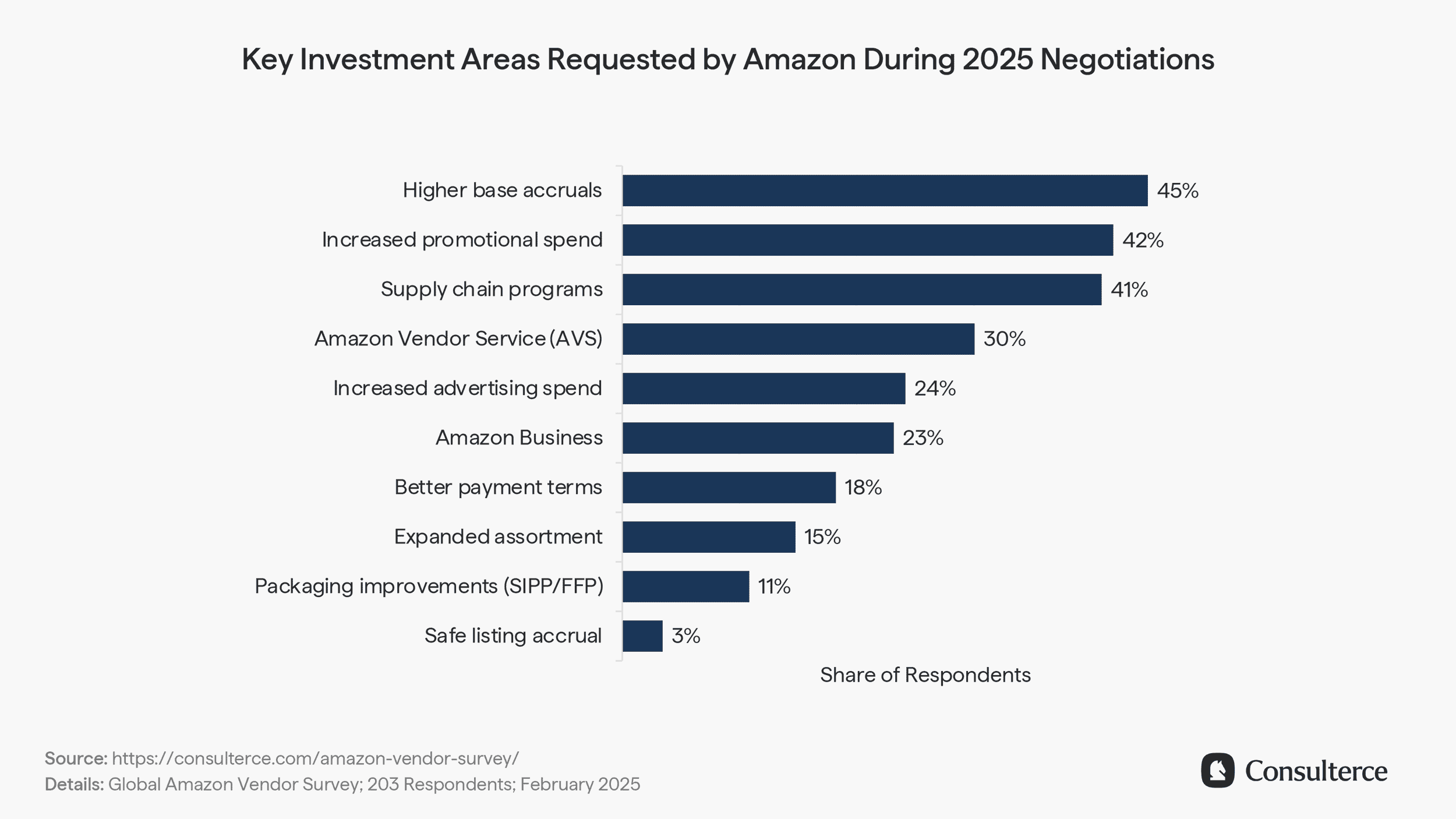

Amazon demands higher promo budgets, base accruals, and the use of supply chain programmes in vendor negotiations

When asked about the key asks from Amazon, participating vendors indicated a strong focus on legacy investment areas. In other words, Amazon lacks new and innovative programs as part of its annual vendor negotiations in 2025.

45% of vendors were asked to invest more in base accruals, such as Automated Marketing, MDF, or Co-op agreements. 42% of vendors received requests to increase their promotional budgets. Another 41% indicated a focus on supply chain improvements from Vendor Managers.

Optimising Retail Media, promotional budgets and portfolio structures are top priorities for 1P vendors

To improve margins with Amazon, 56% of manufacturing brands are looking to improve their Retail Media performance with Amazon.

Another 53% state that optimising their portfolio structure and price-pack architecture will become a top priority in 2025. This includes decisions into the delisting of products as well as the launch of exclusive Amazon assortment.

Mix management was cited as a third priority. 1 in 2 vendors (50%) indicated that directing Retail Media and price promotional activities towards products with an accretive margin position forms a key target with Amazon in 2025.

Conclusion

That wraps up our Amazon Retail study for 2025. I hope you found the data interesting and useful.

If you found value in today's article, please share it on LinkedIn or via email with your coworkers.

And if you participated in the survey, thank you! Without your contribution, this study would not have been possible.

Background of survey and profile of survey participants

The survey was conducted from January to February 2025 and targeted representatives of first-party Amazon suppliers. A total of 203 survey responses were recorded. The survey was conducted anonymously.

Vendor business size with Amazon

38% of survey respondents reported annual Amazon sales between $0 and $10 million. 39% of survey respondents reported annual Amazon sales between $10 and $50 million. 9% of survey respondents reported annual Amazon sales between $50 and $100 million. Another 14% reported annual Amazon sales of over $100 million.

Vendor categories of survey participants

47% of survey participants sell items in the Hardlines goods product family, 45% are actively selling Consumer Goods (Consumables), and 8% were manufacturers in Soft Lines (Fashion, Luxury, and Accessories) categories.

Geographical distribution of survey participants

The survey participants were located in multiple regions. 58% of respondents were located in European markets, 39% in North America, and 2% in Asia-Pacific markets.

Disclaimer

The survey is not and was not sponsored by, run, or affiliated in any way with Amazon.com, Inc. or any of its subsidiaries.